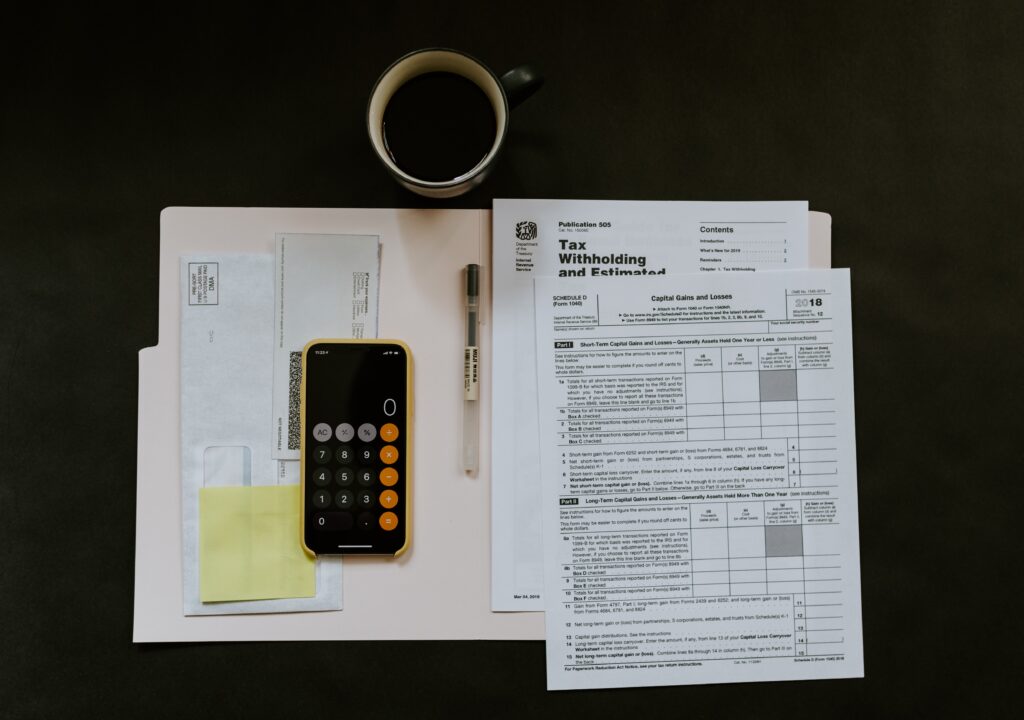

Therefore as we all prepare to file our 2020 tax returns, we wanted to share the common home-related mistakes to watch out for, especially if you are taking any home office tax deductions. Tax pros say these common tax mistakes can cost you money or attract the IRS to your front porch.

1. Deducting the Wrong Year for Property Taxes

Remember that you take a tax deduction for property taxes in the year you (or the holder of your escrow account) actually paid them. Some taxing authorities work a year behind — which means, you are not billed for 2020’s property taxes until 2021. But that’s irrelevant to the feds. Therefore, you need to enter on your federal forms whatever amount you actually paid in that tax year, no matter what the date is on your tax bill. Dave Hampton, CPA, a tax department manager at the Cincinnati accounting firm of Burke & Schindler, has seen homeowners confuse payments for different years and claim the incorrect amount.

Tip: Taking this deduction requires that you itemize.

Make sure to speak with your tax preparer if you prepaid your 2021 property taxes in 2020, given the tax law changes.

- If you had a property tax bill in hand, that means the tax was assessed and you should have been able to deduct it on your 2020 tax return if you itemized.

- If your local taxing authority says it will accept prepayments but the tax hasn’t been assessed, just estimated, the payment likely wasn’t deductible on your 2020 tax returns.

2. Confusing Escrow Amount for Actual Taxes Paid

If your lender escrows funds to pay your property taxes, don’t just deduct the amount escrowed. The regular amount you pay into your escrow account each month to cover property taxes is probably a little more or a little less than your actual property tax bill. Your lender will adjust the amount every year or so to realign the two.

For example, your tax bill might be $1,200, but your lender may have collected $1,100 or $1,300 in escrow over the year. Deduct only $1,200 or the actual amount of property taxes paid that is noted on the Form 1098 that your lender sends. If you don’t receive Form 1098, contact the agency that collects property tax to find out how much you paid.

3. Deducting Points Paid to Refinance

In many cases, you can deduct in full the points you paid your lender to secure your mortgage for the year you bought your home, if you itemize. However, if you pay points in connection with a refinance, you must deduct the points over the life of your new loan.

For example, if you paid $2,000 in points to refinance into a 15-year mortgage, your tax deduction is $2,000 divided by 15 years, or $133 per year.

4. Miscalculating the Home Office Tax Deduction

There are two ways to calculate the home office deduction. One is complicated, has to be recaptured if you turn a profit when you sell your home, and can pique the IRS’s interest in your return. But it also can amount to more of a deduction than the simpler method.

If you don’t care to claim actual costs, which you do under the more complicated method, you can use the simplified home office deduction. If you’re eligible, you can deduct $5 per square foot up to 300 feet of office space, or up to $1,500 per year.

5. Failing to Track Home-Related Expenses

If the IRS comes a-knockin’, don’t be scrambling to compile your records. File or scan and store home office and home improvement expense receipts and other home-related documents as you go.

6. Forgetting to Keep Track of Capital Gains

If you sold your main home last year, don’t forget to report capital gains on any profit above the excluded amounts. You can typically exclude $250,000 of any profits from your income (or $500,000 if you’re married filing jointly).

So, if your cost basis for your home is $100,000 (what you paid for it plus any improvements) and you sold it for $400,000, your capital gain is $300,000. If you’re single, you owe taxes on $50,000 of gains.

However, there are minimum time limits for holding property to take advantage of the exclusions, and other details. Consult IRS Publication 523. And some high-income earners could get hit with an additional tax.

7. Claiming Too Much for the Mortgage Interest Tax Deduction

For the tax year 2020, taxpayers are allowed to deduct mortgage interest on $750,000 of home acquisition debt.

Interest on home equity loans and second mortgages continues to be deductible, but only if the proceeds of such loans are used to substantially improve the home that secures the loan. Interest on home equity loans that were used for other purposes, such as student loans, cars, vacations, are no longer deductible.

And the amount of all mortgage loans (first, second, home equity, and loans for a second home) can’t exceed the $750,000 or $1 million limits.

Please Note: This article provides general information about tax laws and consequences, but shouldn’t be relied upon as tax or legal advice applicable to particular transactions or circumstances. Consult a tax professional for such advice.

]]>Because let’s just be real, there is every day clean, guest clean, and then there’s COVID-19 clean. For that kind of clean you’ll want to break out the tough stuff: bleach, rubbing alcohol, and hot water.

The Best Disinfectants

For your high-touch surfaces, the Centers for Disease Control and Prevention recommends a bleach solution diluted with water, or a 70% alcohol solution.

Here is a bleach diluting recipe to help you know the right balance.

Recipe:

- 5 tablespoons (1/3 cup) bleach per gallon of water

- 4 teaspoons of bleach per quart of water.

Make sure to properly ventilate when disinfecting with bleach.

And check to see if your bleach has expired. Who knew it could? After about 9 months to a year, and if it smells less bleachy, it’s lost its disinfecting power. Time for a new jug.

Important Note: Don’t mix bleach with anything other than water; otherwise, it could set off a dangerous chemical reaction. For instance, bleach + alcohol is a deadly combo.

How to disinfect your home if you don’t have bleach? Regular old rubbing alcohol (isopropyl alcohol or ethyl alcohol) works, as long as it’s at least 70% alcohol, according to the CDC. You can find the alcohol concentration listed directly on the bottle. There is no need to dilute rubbing alcohol, as it is sold in an already diluted state.

Is There a Such a Thing as Too Much Disinfectant?

According to an EPA fact sheet, studies have found that using certain disinfectant products can cause germs to become resistant. The EPA has issued a list of disinfectants on the market that it believes are effective in killing COVID- 19. Look for the EPA registration number on the product and check it against this list to ensure you have a match. Erica Marie Hartman, an environmental microbiologist at Northwestern University in Evanston, Ill., whose research focuses on resistance, confirms soap, bleach, and alcohol are your best bets.

What about the various disinfecting wipes on the market (at least if you can find them)?

Hartman says the active ingredient in many of those is an ammonium compound, which could become resistant to viruses over time.

Surfaces That Need Your Attention

With your preferred disinfectant, wipe down high-touch surfaces like doorknobs, light switches, tables, remotes, banisters, toilets, sinks, and faucets daily or more often, if someone in your home is sick.

Contact time is another key aspect of surface sanitizing. “Disinfection isn’t instantaneous,” says Hartman. [For a bleach solution], you want to leave it on the surface for 10 minutes before wiping it off.”

The CDC has updated its guidance to say that Covid-19 is now thought to be spread most often by respiratory droplets. Although the virus can survive for a short time on some surfaces, it is unlikely to spread from domestic or international mail, products, or packaging.

However, people may be infected by touching a surface or object that has the virus on it and then touching their own mouth, nose, or eyes, even though this is not believed to be the main way the virus spreads.

Can I Use Bleach on My Floors?

For your nonporous floors, like those in the bathroom, the CDC recommends mopping with the bleach solution.

Avoid bleach on hardwood and other porous floors because of staining. Instead, use a disinfecting wet mop cloth without bleach.

Cleaning vs. Disinfecting

Disinfecting with bleach isn’t actually cleaning. If you also need to clean your countertops of dirt and grime, do that first with soap and water. Then use the bleach solution or rubbing alcohol to combat the virus.

Killing Microbes on Clothes

Most washing machines today do a bang-up job on dirty clothes with cold water, which is best for energy savings. But if you have a sick person in your house, the hot-water setting followed by a high-heat dry for about a ½ hour to 45 minutes is best for virus eradication. Don’t forget about your laundry hamper. Wipe it down like you would other surfaces. You can also use a reusable liner bag, which you can launder with the clothes.

What If I’m Selling My House, Am I Inviting More Germs In?

How to disinfect your home when it’s for sale? Virtual showings and tours are the ideal, and your agent can set those up.

However, if there’s a need to have someone come in, talk to your agent who will work with you to establish a hygienic protocol, including requiring visitors to wash hands with soap and water or use hand sanitizer when they arrive, and to remove shoes or wear booties before entering. Removing shoes not only reduces dirt coming in, but potentially germs. After any showings, practice your surface wipe-down routine.

Finally, when you work with disinfectants, practice some self-care. “Alcohol and bleach can be very aggressive on your skin, so wearing rubber gloves can help protect your hands,” Hartman says.

Originally written by: Christina Hoffmann

]]>Here are a few tips on how to keep the peace while house hunting.

Before you and your partner start sending each other links to the home of your dreams, have a few conversations about the home buying process.

A couple buying a house should talk about money, of course, but also about their expectations for their first home. Talking now will keep you productive, positive, and focused on finding the right house. It will also help you prevent house-buying stress from affecting your relationship.

OK, we’re about to get a little “Modern Love” here.

1. Get On the Same Page About Expectations

No matter how connected you two are, there are still unspoken and undefined expectations between you. Especially when it comes to a couple buying a house. Buying a home can reveal relationship problems, because it’s the biggest financial transaction you’ll make, and there are a lot of emotions and expectations tied up in the idea of home.

Listen to your partner and commit to the idea that each person has a voice in every issue.

“That would be my No. 1 principle,” says Donna R. Baptiste, a licensed marriage and family therapist, and professor at Northwestern University’s Family Institute. “Two people must respect each other’s right to have a say.”

How to start? Ask questions like:

• Why do you want to buy a house?

• What’s the most important thing to consider, in your opinion?

• How long do you want to live there?

• Do you want something perfect or a fixer-upper?

• What do you think our budget should be?

2. Be Prepared to Back Down

Not every decision will be 50-50. “Equal say is not always the standard,” Baptiste says.

But both of you should be willing to accept no for an answer. This prevents gridlock. And ceding some control makes the decision on which home to buy a shared one.

Consider the situation faced by work-from-home clothing designer Veronica Sheaffer and her husband, teacher Keith Dumbleton. They bought their prewar apartment on Chicago’s far North Side four years ago.

While scrolling through listings, Sheaffer fell for the property’s vintage millwork and spacious layout, but the building was 12 miles from the centrally located neighborhood they’d been living in. Sheaffer accepted the hours the new location would add to Dumbleton’s school commute could be a deal breaker.

“I gave him the power of refusal and prepared myself for losing the place,” she says. Knowing that Sheaffer was conscious of the sacrifices he’d be making, Dumbleton agreed to move forward with making an offer. “Her being open to me saying no allowed me to make that decision, and I don’t regret it.”

3. Do Scenario Planning

New homes have a way of changing life’s routines.

Does one of you take the dog out? If so, that beautiful sixth-floor walk-up may affect the dog caretaker’s mornings (and moods). Does one of you do most of the outdoor chores? How do you really feel about taking care of a massive lawn? That house that sits on top of a hill is gorgeous, and the views! But will you like hauling bags of groceries up the three flights of

stairs to the front door?

“I ask a couple to have it sink in,” says Dan Sullivan, a REALTOR® at Compass in Chicago. “What is it going to physically be like living in that property, day in and day out?”

The more you think it over together, the happier you’ll both be after you move in.

4. Ask An Expert

As a couple buying a house, you may be in full agreement or you may be at an impasse, but either way talk to a real estate agent and, as Baptiste recommends, “submit to the idea of getting good advice.”

A good agent is like a reference librarian and a personal coach in one. They can help you navigate the home buying process minutiae, like finding a good mortgage broker or dissecting the details of a home inspection.

An agent can give you the knowledge you need to make a wise decision. And they can pump you and your partner back up when your energy has subsided because you’ve looked at 22 houses and not seen one worthy of an offer. Or you put in an offer and it fell through.

Leaning on a professional to offer perspective and help work through disappointment releases some buying-a-house stress on a relationship. “As much as possible, as early as possible, I try to get [couples] to see the big picture,” Sullivan says.

5. Recognize You’re a Team

Involving an agent in the home buying process can have another unexpected outcome, says Sheaffer. It brought her and Dumbleton closer together.

Having the agent participate in discussions — and even occasionally disagreeing with her — “helped us [see] that we know each other, we know our lifestyle. Anything that will allow you to bond more with your partner is always positive.”

The agent got them to talk to each other about what they wanted and didn’t want in a house. It helped them hash out their likes and dislikes, constructively.

Instead of letting buying a house lead to relationship problems, turn the experience into a chance to learn and grow together. Talk. Listen. And get good advice from a smart agent. You’ll end up as homeowners — with an even better connection.

What’s not to love?

Originally article written by: HouseLogic

If you found this article helpful, feel free to leave your comment below. Tell us what you liked or disliked, and what you would like to see more of.

]]>Technology and good-old-fashioned creativity are helping agents, buyers, and sellers abide by COVID-19 health and safety practices while getting deals done.

Some buyers are touring houses virtually. Others visit in person while remaining at least six feet from their agent. Sellers are hosting open houses on Facebook Live. Appraisers are doing drive-by valuations. Buyers are watching inspections via video call. Masked and gloved notaries are getting signatures on doorsteps.

“We have had to make some adjustments, for sure,” says Brian K. Henson, a REALTOR® with Atlanta Fine Homes / Sotheby’s International Realty in Alpharetta, Ga. “Everyone is trying to minimize face-to-face interactions. There have been some delays, but mostly, deals are getting done, just with tweaks.”

Here is what you can expect if buying or selling a home during this pandemic.

Virtual Showings

Regulations regarding in-person showings vary by city, county, and state. Some states are allowing them and some have ban them. Therefore, it is important to check with your state, county, and local government to get the latest on business closures and shut-down rules.

Agents have conducted home tours via FaceTime and other similar tools for years. But these platforms have become invaluable for home buying and selling during the pandemic. Real estate sites report a surge in the creation of 3D home tours. Redfin, a real estate brokerage, saw a 494% increase in requests for video home tours in March 2020.

“I’ve done several FaceTime showings,” says Henson. He conducted virtual showings before COVID-19, too. He recently closed a deal on a home the buyers only saw on video, he says, but hasn’t yet done so during the pandemic.

In places where in-person showings are allowed, agents wipe down door handles, spray the lockbox with disinfectant, and open up the house, closets, everything for a client. “We leave all the lights on so no one touches switches, and we don’t touch cabinets or doors during showings,” Henson says.

Recommendations For Safe Showings

The NATIONAL ASSOCIATION OF REALTORS®, which produces HouseLogic, recommends only one buyer enter a home at a time, with 6 feet between each guest. NAR also recommends agents have potential buyers wash their hands, or use hand sanitizer when they come in the door. They should also remove their shoes. In addition, no children should be present at showings.

Changes to Down Payment Assistance

Many organizations have temporarily suspended offering down payment assistance to first-time home buyers or they have changed the rules. As a first time home buyer, you can check the status of programs in your area at the Down Payment Assistance Resource site.

Desktop, Drive-By Appraisals

Appraisers are essential workers in many areas, so home valuations are continuing. But often remotely. New, temporary rules from the Federal Housing Finance Authority allow drive-by and desktop appraisals for loans backed by the federal government.

In a desktop appraisal, the appraiser comes up with a home estimate based on tax records and multiple listing service information, without an in-person visit. For a drive-by, the appraiser only looks at the home’s exterior, in combination with a desktop appraisal. The Appraisal Foundation has put out guidelines for handling appraisals during the pandemic.

You can find more information on their website: https://www.appraisalfoundation.org/

On the other hand, some private lenders still require in-person appraisals, which are allowed even in areas with shutdown orders. Private lenders hold about 35% of first-lien mortgages, according to the Urban Institute.

When appraisers come to your home, they should adhere to CDC guidelines, including wearing gloves and a face mask, keeping at least 6 feet apart from anyone in the home, and asking if the homeowners have been sick or traveled recently to a COVID-19 hotspot.

Inspections Via Live Video

Inspectors are now often working alone, no buyers in tow, and using hand sanitizer and alcohol wipes. The National Association of Certified Home Inspectors advises inspectors to videotape their inspection so clients can watch it at home later, or to use FaceTime or other live video chat apps to take their clients along on the inspection, virtually. They can also call clients with their findings after they’re done.

The American Society of Home Inspectors has also issued guidelines for inspectors so they keep themselves and the homeowners safe while providing an accurate assessment of a home’s condition.

Mortgage Rates and Locks

With mortgage rates fluctuating quickly and closing times taking longer than usual, some lenders are extending mortgage rate lock periods. You can grab a good rate and hang on to it even if your lender takes longer than usual to process your loan.

But the protocol depends on the lender and the loan. Some lenders are offering this for all loans; others only for refi’s. Check with your lender about its policy.

Employment Verification

An important step in getting a mortgage is proving the borrower has a job. In pre-coronavirus days, lenders called the borrower’s employer for a verbal verification. The Federal Housing Finance Authority, which oversees Fannie Mae, Freddie Mac, and federal home loan banks, has relaxed the rules for loans backed by the federal government because so many businesses are closed.

Lenders for federally backed loans now accept an email from an employer, a recent year-to-date paystub, or a bank statement showing a recent payroll deposit as proof of employment.’

Walk-throughs

Home buying and selling during the pandemic means real estate agents can conduct the final walk-through via video with their clients. Or they can just open the home and have buyers walk through on their own. Henson says he still accompanies his clients, but stays six feet away and has them wash their hands when entering and exiting the house. Everyone’s wearing masks, too.

And, of course, when the buyers take possession, they should disinfect prior to moving in.

Remote Notarization – Dependent on Location

About one-half of states have permanent Remote Online Notarization (RON) policies. These allow a notary and signer in different locations to sign electronic document, usually by use of video apps like Zoom or FaceTime. Notaries will watch you sign either a paper document or do an electronic signature on an e-doc, via camera.

Some states have rolled out temporary rules allowing RON. The number of states allowing remote notarization could grow as federal and state pandemic legislation expands.

Closings With A Twist

Traditional closings, where everybody gathered around a big table to sign the final papers, are no longer possible. Title companies and banks are getting super creative in dealing with the limitations.

A Minnesota company, Legacy Title, rolled out a drive-thru closing service at one of its offices in an old bank branch building. The title company rep sits in a bank teller window and handles the closing papers while the customer sits in their car. Legacy completed 14 closings in the first week it offered drive-thru service.

Then there are drive-by closings, where the entire transaction takes place in cars. Masked and gloved notaries meet buyers in parking lots and pass documents through car windows.

TIP: Find out if your county recording office can complete the deal online.

Student Loan Relief

Finally, if you’re also trying to swing your student loan payments, know that federal student loan borrowers get an automatic six-month break in loan payments from April 10, 2020, through Sept. 3, 2020. Thanks to the Coronavirus Aid, Relief and Economic Security (CARES) Act, they also won’t be charged a dime of interest in that time.

Learn more at the Consumer Finance Protection Bureau’s site: https://www.consumerfinance.gov/

Keep in mind that payment suspension only applies to federal loans owned by the Department of Education. Some help may be available to borrowers with private student loans and other loans (like Perkins Loans and Federal Family Education Loans) that aren’t covered. Reach out to your student loan servicer for information.

Should You Buy or Sell?

As a home buyer or home owner, the decision to buy or sell is a big decision. It is an even bigger decision with the addition of a pandemic. The real estate industry is creatively and safely responding to the situation, and mortgage rates remain low. Your agent is a great source of information about home buying and selling during the pandemic to help you feel comfortable. But, ultimately, it’s a question only you can answer.

Originally written by: Leanne Potts.

Have you bought or sold a home during the pandemic? What is your experience? We would love to hear from you, comment below!

]]>

There are so many steps from the first decision to buy a house to the time you are handed the keys to your home.

How long is the house buying process? The timeline depends on the availability of homes and the amount of time you spend shopping for one. But once you have a contract, it takes an average of 50 days to close on a house.

There are a lot of steps to buying a house, and any of them could drag out the timeline, especially if you’re not prepared. Here’s the home-buying timeline, broken down step-by- step.

1. Know Before You Go

Time: 1-14 days

Dreaming about owning your own home is one thing; making your dream a reality is another. To get beyond the dream stage, you must take the time to learn the steps and the important roles of each professional play in making this as pain free as possible.

The most disappointing feeling is to fall in love with a house only to discover you cannot afford it. Going through the pre-qualification process with your bank or mortgage consultant would help you to identify your spending power. Although pre-qualification does not guarantee you will be given the loan by that specific lender, it does give you an idea of how much you can afford to spend on your dream home.

2. Real Estate Agent Selection

Time: 1-7 days

Selecting a Real Estate Agent is paramount in your home buying process. Real estate agents can provide many useful services and work with you in different ways. In some real estate transactions, the agents work for the seller (Seller’s Agent). In others, the buyer may have his/her agent (Buyer’s Agent) and sometimes the same agent works for both the buyer and the seller (Dual Agent). It is important for you to know the role the agent is playing.

Once you have agreed (either orally or in writing) for the firm and its agents to be your buyer’s agent, they may not give any confidential information about you to sellers or their agents without your permission so long as they represent you. But until you make this agreement with your buyer’s agent, you should avoid telling the agent anything you would not want a seller to know.

Let friends and family know that you are house hunting – they may tell you about a house before it is listed (someone in their neighborhood is going through a divorce and will not stay in the home, family being relocated, older homeowner cannot maintain their home any longer and needs to downsize).

Take a Sunday afternoon drive or walk through the neighborhoods you desire. Ask others any questions you may have.

Ask lots of questions of the homeowner, seller or broker about the house – when was it built and bought, why the sale is being made, how long has the house been on the market, what major work has been done to the house and when and why, any major problems in the area/neighborhood, etc…

Try traveling (driving or public transportation) from your intended neighborhood to and from work during rush hour to experience what it would be like when you start living there.

3. Loan Pre-Approval

Time: 5-8 business days

Most buyers will have to finance their home by obtaining a home mortgage from a lending institution. Having a pre-approval before you go house hunting is a strong signal to your realtor and sellers of your seriousness to purchase. Compare your down payment options, calculate how much home you can afford and compare lenders to get a reliable quote.

There are two terms you should be aware of, pre-approval and pre-qualification.

Prequalification is an early step in your homebuying journey. When you prequalify for a home loan, you’re getting an estimate of what you might be able to borrow, based on information you provide about your finances, as well as a credit check. Prequalification is also an opportunity to learn about different mortgage options and work with your lender to identify the right fit for your needs and goals.

Preapproval is as close as you can get to confirming your creditworthiness without having a purchase contract in place. You will complete a mortgage application and the lender will verify the information you provide. They’ll also perform a credit check. If you’re preapproved, you’ll receive a preapproval letter, which is an offer (but not a commitment) to lend you a specific amount, good for 90 days.

Getting preapproved is a smart step to take when you are ready to put in an offer on a home. It shows sellers that you’re a serious homebuyer and that you can secure a mortgage – which makes it more likely that you’ll complete your purchase of the home. Pre-approval goes deeper than pre-qualification. You may be asked for pay stubs, tax returns, W-2 statements, bank account information and credit report. It is best to have these documents organized before you have your meeting with the lender.

Compare rates from lenders within a 14-day window: Credit bureaus will count all their checks as just one. (That’s good news for your credit score.)

4. House Shopping

Time: A few days to a few months

Now that you know your purchasing power, you can go shopping. Now is the time to determine your needs/must haves and wants/not necessary. There are so many variables, needs such as the school system, the neighborhood, distance from you family, must be prioritized over a swimming pool, countertops or condition of doors and windows.

Before starting your hunt for a new home, it is advisable to make a list of all your basic needs and desires while targeting the most important ones. Making a list and highlighting what truly matters is the way to go. On top of it all, it will make the hunt easier, but at the same time, you need to know that it’s nearly impossible to have all items checked.

5. Offer, Negotiate, Attorney Review Period and Fully Executed Contract

Time: 1-7 days

Work with your agent on price, contingencies, and other terms of the deal. After the offer is made and accepted, the attorneys for both sides review the contract and solidify the agreement.

A couple of tips to help make this step proceed smoothly:

- Include the pre-approval letter from your lender in the offer and put down earnest money. (Commit 3% to 4% of the sale price instead of the standard 1% to 3%, and you might really put a fire under them.)

- I always ask my buyers to write a letter to the seller thanking the sellers for allowing them (the buyers) to be the purchasers of the home and expressing why they would love to be the new owners of their home. Keep in mind, this is a personal item the sellers are parting with, personalizing the offer makes a huge difference.

- If you receive a counteroffer, respond ASAP. You don’t want to give another buyer time to jump in with a better offer.

6. Final Mortgage Approval

Time: A few days to 3 weeks

Getting pre-approved for a mortgage doesn’t automatically mean you get a loan on the home you have under contract. The lender has a few other requirements once the home is chosen, such as an inspection and appraisal. And they’ll want to see even more current copies of your financial documents.

From this point on, the steps to buying a house will often overlap, so you’ll have several wheels in motion.

You will also begin to start spending money of the pre-purchase items like home inspection, appraisal, and insurance.

7. Home Inspection

Time: 3-7 days to schedule; 2-3 hours to inspect

Don’t expect perfection. There is no perfect home. Even new construction may have flaws. As soon as your contract is accepted, contact an inspector to get on their books. The inspection itself will only take two or three hours, and I highly recommend you be present with a note book the entire time. Feel free to ask a lot of questions.

The inspection report may take two to three days to be completed with pictures and descriptions of each part of the inspection. All reports are done digitally and sent to you and your attorney for review.

If the inspection turns up issues, it can cause some delays or a need for additional inspections. The issues may also result in further negotiations with the seller through your attorney. For example, if the inspection reveals termites, the seller may have to call in a pest control company and have the termites treated and provide proof of this treatment to you and your attorney.

8. Home Appraisal

Time: Up to 5 days to schedule; a few hours to do the appraisal; up to 5 business days to get the report to the lender

The appraisal is key to getting a mortgage. If the home fails to appraise for the mortgage amount, you may have to increase your down payment or renegotiate a lower price with the seller. That’s why you want to line up an appraiser as soon as you have a house under contract. And unlike the home inspection, this report goes to the lender instead of you and takes longer because the appraiser has to do additional research on what homes are selling for in the area.

9. Title Insurance

Time: 1-3 business days for title check; 2 weeks for insurance policy

A big part of securing title to a property is to conduct a thorough search of the property’s history. The title company will work to locate, prevent, and eliminate any risks or losses which may arise due to title problems, using public records to establish a clear chain of ownership and disclosing all identifiable outstanding claims against it.

10. Homeowners Insurance

Time: Up to 2 weeks

Your insurance company may send someone to the property to assess for potential risks. Your mortgage lender may require other things like a new roof or other types of coverage, such as flood insurance.

11. Closing Part Two

Time: A few minutes to a few days

Your title company and/or attorney will let you know whether you need to bring a cashier’s or certified check or wire your funds for closing and to whom it should be payable to. Be very mindful of wire fraud when sending money. Transfer the funds to the right account and get your money ready to release and confirm the recipient’s information.

If you ever receive wiring instructions by email, call your agent or lender to confirm one of them sent it. Call the phone number you have on record for your agent, not the one listed in the suspect email.

12. Conduct a Final Walk-Through

Time: 1 hour, the day of or day before closing

Keep in mind this is your largest investment. On the day of the closing return to the house and walk around and through the house to make sure the sellers made any agreed-upon repairs and left the property in as good (or better!) condition than the last time you saw it.

If things are not the way you expected them to be, you must let your closer know before proceeding.

13. Closing

Time: 50 days on average; 1-2 hours to actually sign the paperwork

Each step after you’ve got a contract on a home is part of the closing process. And that process — which includes getting the loan, inspection, appraisal, title, insurance, etc. takes the average home buyer about six weeks.

On the day of the closing, what with two forms of government issued IDs such as driver’s license, US passport, US passport card or social security card. Be prepared to sign between 80-100 pages. The total signing time is between 45 minutes and 1 hour. It is worth it because the handover of the keys takes no more than 1 minute.

14. Locks

Always! Always! Always! Change the locks on the outer doors. Keep in mind the amount of people who had access to the house through the former owners, the realtors and contractors. Changing the locks will give you peace of mind.

]]>